| 🌝 Бренд | Vavada |

| 🌝 Официальный сайт | |

| 🌝 Рабочее зеркало | Актуальное зеркало - перейти на зеркало |

| 🌝 Платформы | iOS, Android, Windows |

| 🌝 Количество игр | 3600+ |

| 🌝 Языки | RU, EN |

| 🌝 Саппорт | Live-чат, контактный телефон, skype, email |

| 🌝 Мин. депозит | 50 RUB |

| 🌝 Мин. вывод | 1000 RUB |

Рабочее зеркало Вавада

Зеркало - это копия официального сайта, которая работает под другим доменом. Это связано с тем, что Роскомнадзор принуждает интернет-провайдеров блокировать официальный сайт, т. к. в стране действует ФЗ-244. Согласно этому закону, в России запрещена деятельность любых онлайн-казино. Поэтому для работы на территории РФ, компания предлагает игрокам альтернативный вариант - рабочеесейчас зеркало Вавада. Оно функционирует на стороннем прокси-сервере, следовательно, не попадает под действующий закон. Из отличий альтернативного заведения от официального - только несколько деталей:

- адрес отличается доменным именем: к альтернативной ссылке часто добавляются дополнительные элементы (буквы, дефисы, цифры и их комбинации);

- прокси официального заведения - .com, а у копии он другой: .ru, .vip, .bet или любой схожий;

- продолжительность работы одного актуального зеркала Vavada com зачастую не превышает 4 недель, так как такие ресурсы блокируются РКН.

В остальном расхождения заканчиваются: функционально заведения на 100% идентичны, у них повторяется дизайн, они используют одну информационную базу (допускается игра с одного акка на двух порталах), в них предусмотрены те же разделы, бонусы и софт. Но для игры через зеркало Вавада придется часто искать новые адреса. Ссылки на них публикуются в социальных сетях бренда, поэтому стоит подписаться на их рассылку. Альтернативный адрес можно запросить у техподдержки клуба или самостоятельно поискать, изучив выдачи в поисковиках. Часто ссылки размещаются в рекламных материалах, опубликованных брендами-партнерами.

Для использования зеркала нет необходимости устанавливать дополнительный софт, оно бесплатное, работает стабильно, а при наличии аккаунта пользователю не нужно создавать новый профиль. Если же его нет, то процедура регистрации учетной записи полностью идентична той, что предусмотрена на официальном сайте.

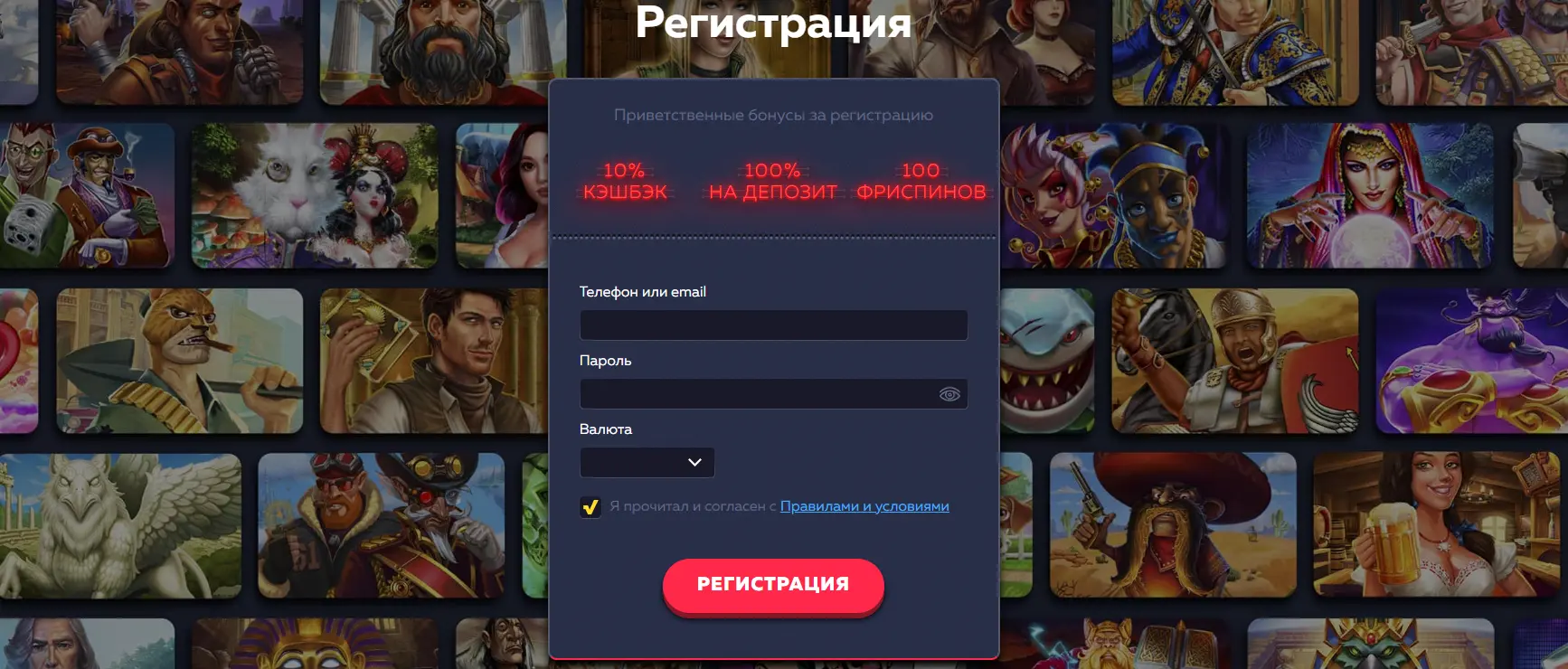

Регистрация в Вавада: вход в личный кабинет

Чтобы создать аккаунт в casino, посетителю должно быть более 18 лет. При регистрации запрещено использовать личные данные третьих лиц и недействительные документы. Недопустим мультиаккаунтинг. В остальном регистрация в Вавада состоит из нескольких действий:

- Переход на официальный сайт и нажатие на Регистрация.

- Указание email-адреса или номера телефона.

- Выбор игровой валюты + ознакомление и принятие условий пользования сервисом.

- Указание пароля.

- Завершение процедуры подтверждающей кнопкой.

Как только эти действия выполнены, на электронную почту придет письмо. Пользователь должен открыть его и перейти по полученной ссылке. Если же создание акка проводилось через телефон, то в разделе Профиль", нужно нажать Получить код, а после ввести шифр в специальное поле. Аккаунт будет создан и подтвержден.

При необходимости на официальном сайте Vavada можно подключить двухэтапную аутентификацию, заполнить пустые поля в блоке Профиль и пройти процедуру верификации. Все эти процессы не обязательны и проводятся по желанию. Если же гемблер желает подтвердить свою личность, ему необходимо прислать представителям казино скан своего паспорта или любого документа, удостоверяющего личность. Сделать это нужно через Профиль - Верификация. Проверка занимает до 24 часов.

Бонусы и промокоды Вавада

Бонусная политика компании разнообразна, поэтому здесь найдутся награды для всех членов ресурса. Зарегистрировав аккаунт, каждый пользователь получает приветственный набор фриспинов, а за первое пополнение баланса на счет возвращается до 100%. Активно играя, клиенты накапливают определенный объем ставок, повышая свой статус в программе лояльности. Это дает им ряд привилегий. Дополнительно предусмотрены промокоды Vavada и кэшбек.

Бонус за регистрацию

Регистрируя аккаунт, новички награждаются 100 фриспинами для автомата Great Pigsby Megaways. Активы выдаются автоматически. В срок до 14 дней с момента их получения поощрения нужно потратить и отыграть. Вейджер равен х20 раз.

Следующая часть welcome-акции - 100% бонус Vavada на депозит. Возврат предоставляется новичкам на следующих условиях:

- минимальный депозит - ₽50 и более;

- максимальный возврат - 100 000 рублей;

- вейджер - х35;

- на выполнение отыгрыша дано 14 дней.

Максимальный коэффициент выигрыша с бонусных активов - х10 от фрибета. Сразу после выполнения условий отыгрыша все средства переводятся на основной счет.

Программа лояльности

Система лояльности в клубе состоит из 6 уровней. Подъем по каждому из них должен сопровождаться накоплением определенного объема трат за отведенный период. Так что чем больше пользователь совершил ставок в Вавада за месяц, тем выше его статус в Loyalty program и награды. Из привилегий: предоставляется личный менеджер поддержки, повышаются лимиты на кэшаут, открывается доступ к более премиальным турнирам.

|

Звание |

Ежемесячная сумма пари, $ |

Ежедневный лимит, $ |

Ограничение в неделю, $ |

Лимит в месяц, $ |

|

Новичок |

0 |

1 000 |

5 000 |

10 000 |

|

Игрок |

15 |

1 000 |

5 000 |

10 000 |

|

Бронзовый |

250 |

1 500 |

7 000 |

15 000 |

|

Серебряный |

4000 |

2 000 |

12 000 |

20 000 |

|

Золотой |

8000 |

5 000 |

20 000 |

30 000 |

|

Платиновый |

50000 |

10 000 |

50 000 |

100 000 |

Кэшбек

Размер ежемесячного кэшбека у casino фиксирован, и он равен 10% от потраченных средств. Сумма возврата полностью зависит от объема потраченных денег. Если же гемблер в одном месяце выиграл больше, чем проиграл, кэшбек ему не предоставляется. Но в следующем месяце, если пользователь выполнил условия, ему снова начисляется возврат. Вейджер для этого предложения - х5. Все начисленные поощрения можно потратить в лучших автоматах заведения.

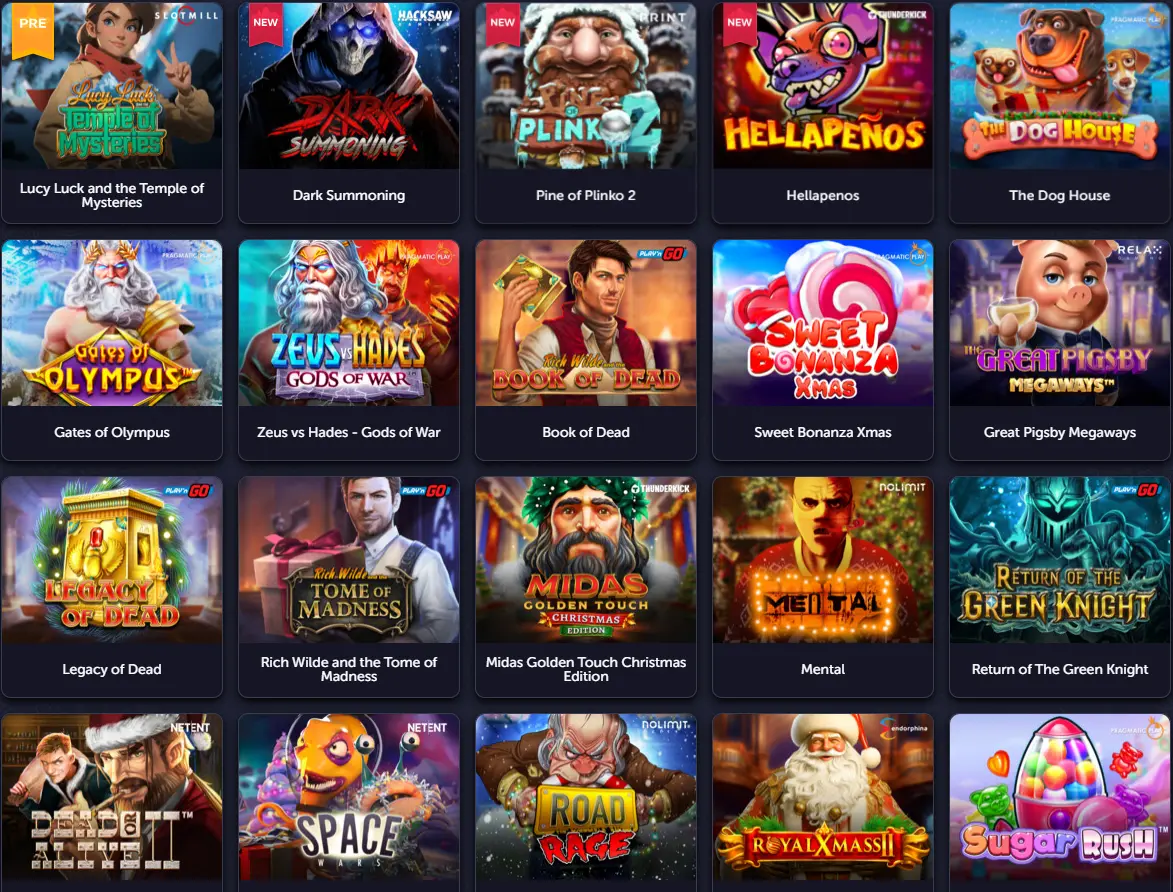

Коллекция игр Vavada Casino

Одно из важных достоинств проекта - сотрудничество с 50+ компаниями-провайдерами. Среди этих брендов есть как новые, так и популярные имена: Vivo Gaming, IgroSoft, Evolution, Microgaming, Playtech, Pragmatic Play. Софт состоит из лайв-релизов, слотов Vavada, настолок, аркад, карточных и краш развлечений. Всего больше 4800 наименований: от классики до современных многофункциональных аппаратов. Встроены фильтры по новинкам, популярности, производителю. Есть поиск по названию + вкладка Избранное. Дополнительно автоматы Вавада оснащены режимами реальной игры и демо.

Бесплатный софт

Функция Демо позволяет попробовать релизы бесплатно. Чтобы сыграть в бесплатном формате нет необходимости в регистрации учетной записи - достаточно выбрать автомат и найти на нем надпись Демо Vavada. Нажав на этот блок, аппарат запускается, и игрок может разобраться в его функциях, особенностях и правилах, не рискуя собственными финансами. Если же активы закончились, нужно просто обновить страницу. Практически 100% слотов Вавада оснащены такой функцией, остальные же категории предлагают режим в большинстве своих продуктов. В их число входит категория Live.

Но, используя бонусные активы, у клиентов компании нет шансов заработать реальные деньги или выиграть один из джекпотов:

- Major - 425 000+ долларов США;

- Mega - почти 5 500 USD;

- Minor - более $100.

Помимо них казино Вавада ежедневно разыгрывает тысячи других мелких призов. Они распределяются случайным образом, поэтому у каждого члена клуба есть шанс получить что-то ценное вне зависимости от суммы пари. Живые развлечения также разыгрывают все вышеописанные поощрения.

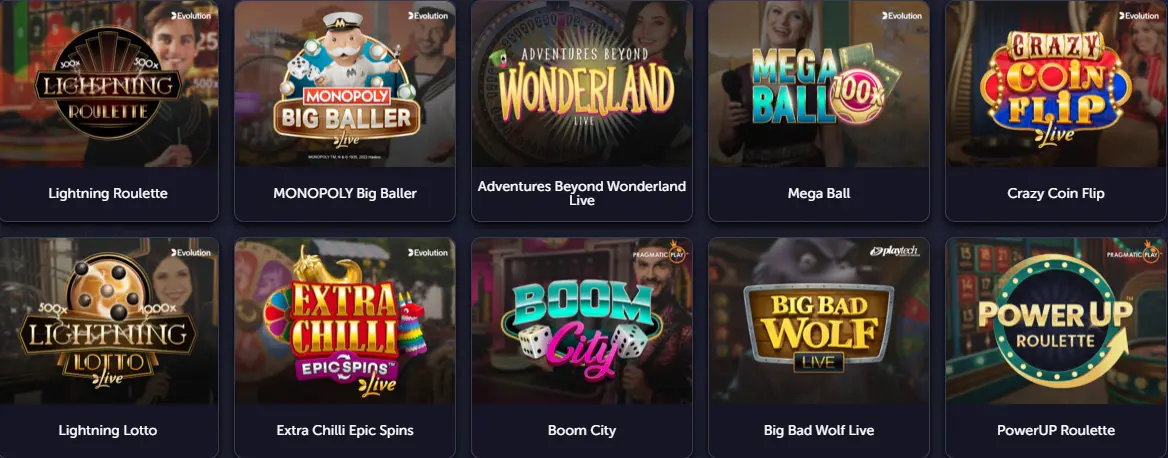

Лайв предложения

Live-релизы - это развлечения в живом формате. В таких предложениях всем процессом управляет настоящий ведущий, а игровые сессии проводятся онлайн. Участники сидят за монитором своего ПК или смартфона и могут общаться друг с другом через чат. Вся игра проводится в режиме реального времени, а все действия ведущего передаются через камеру на мониторы участников. Среди развлечений данной категории: несколько игровых автоматов, блэкджек, колесо фортуны, кости, рулетка и другие. Всего около 120 предложений разных тематик и видов. Вот лишь некоторые топ слоты Вавада в категории live:

- Mega Wheel: слот от Pragmatic Play, созданный по мотивам Money Wheels и Big 6 в 2020 году. Потенциальный джекпот - х500 от размера ставки; лимиты - от 10 центов до 1000$; RTP - 96,5%. Правила: колесо состоит из 56 сегментов, где на каждом из них изображены числа. Гемблер должен угадать сегмент, на котором остановится стрелка колеса после его запуска.

- Dragon Tiger: автомат Вавада на деньги от Evolution Gaming, созданный в тематике китайских символов в конце 2020 года. Максимальный приз - х20000 от размера пари; лимиты ставок - от 0.2 до 100$; RTP - 95.5%. Слот состоит из 4 линий и 5 барабанов. Правила: добиться совпадения символов или выпадения бонусных функций.

Adventures Beyond Wonderland Live: аппараты от Playtech, созданный по мотивам книги Приключения Алисы в стране чудес в 2021 году. Самая крупная награда - 500 000 фунтов стерлингов; ограничения по суммам - 0.2 до 1000 долларов США; RTP - 96.82%. Правила: колесо фортуны состоит из 56 сегментов, нужно угадать ту ячейку, где колесо остановится после прекращения своего вращения.

Турниры Vavada

Следующий важный блок - турниры. Они условно поделены на несколько типов, каждый из которых определяется целью состязания: выбор счастливчика, исходя из максимального джекпота, полученного с фриспинов; определение победителя на основании общего объема ставок за отведенный период; награждение пользователей, получивших наибольшее количество очков из расчета выигранных сумм со ставок с коэффициентами х100. Примеры турниров по их типам: Silver freespins tournament, Maxbet и X-Plus.

Общий призовой фонд у каждого состязания свой и именно он устанавливает количество потенциальных счастливчиков. Так победителями могут стать от 30 до 120 лучших игроков турнира Вавада -у каждого соревнования количество призеров разное. Среди разыгрываемых наград - денежные призы и автомобили.

Чтобы присоединиться к тому или иному состязанию нет необходимости в подаче заявок, ведь все члены клуба принимают участие в них автоматически. Но выбор соревнований определяется рангом в программе лояльности каждого отдельно взятого клиента. Чем он выше, тем больше соревнований будет доступно: так игроки со статусом Gold могут принимать участие во всех турнирах для их статуса и тех, что ниже. Но им не будут доступны состязания для категории Платиновый.

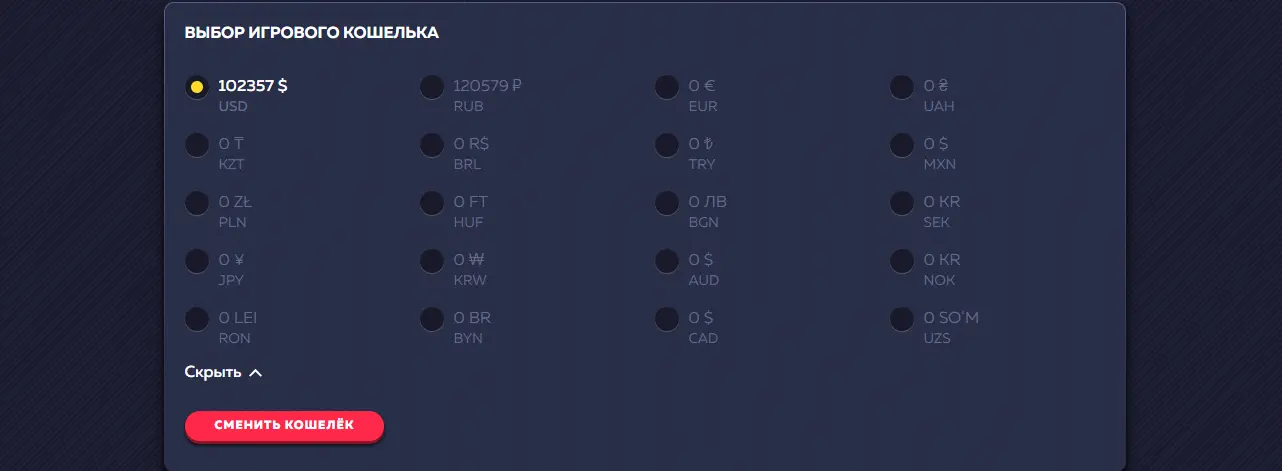

Кошелек

Компания Вавада 2024 - это международное казино, которое принимает гемблеров из разных стран. Поэтому ресурс поддерживает 26 валют и предоставляет 32 платежные системы. Некоторые из них доступны, исходя из ГЕО посетителя. Из основных платежек выделяются базовые варианты (Visa, Piastrix, Neteller) и более современные (BTC, SMS, iPay). Вот небольшой список методов, актуальных для каждого юзера casino:

- USDT, ETH, BTC, XRP, LTC, BNB;

- MasterCard и Visa;

- Piastrix, Skrill, Sepa, Neteller;

- SMS, Jeton, MuchBetter.

Чтобы пополнить баланс, следует открыть вкладку Пополнить, выбрать платежную систему и кошелек, указать сумму, вписать платежные данные. Минимальный размер депозита - от 50 российских рублей, а максимальный не установлен. Время ожидания варьируется в зависимости от платежной системы: для крипты - от пары минут до получаса, для других вариантов - от 30 минут до 4 часов.

Чтобы оформить заявку на кэшаут в Online Casino Vavada, следует открыть тот же раздел, но перейти во вкладку Вывести. Дальше выбрать метод, вписать сумму, установить валютный кошелек и внести платежные данные. Минимальный размер на вывод - ₽1000, а максимальный стандартно - 100 000 RUB в сутки. Однако ограничения зависят от статуса лояльности, поэтому их можно увеличить вплоть до 1 млн. рублей в день. Зачисления на банковский счет для криптоактивов проводятся в течение 2 часов, а через другие системы увеличиваются до 6 часов. Если же кэшаут заказан в выходные или же праздничные дни, все гемблеры ограничены выводом в 200 000 рублей в сутки.